Deepoption01

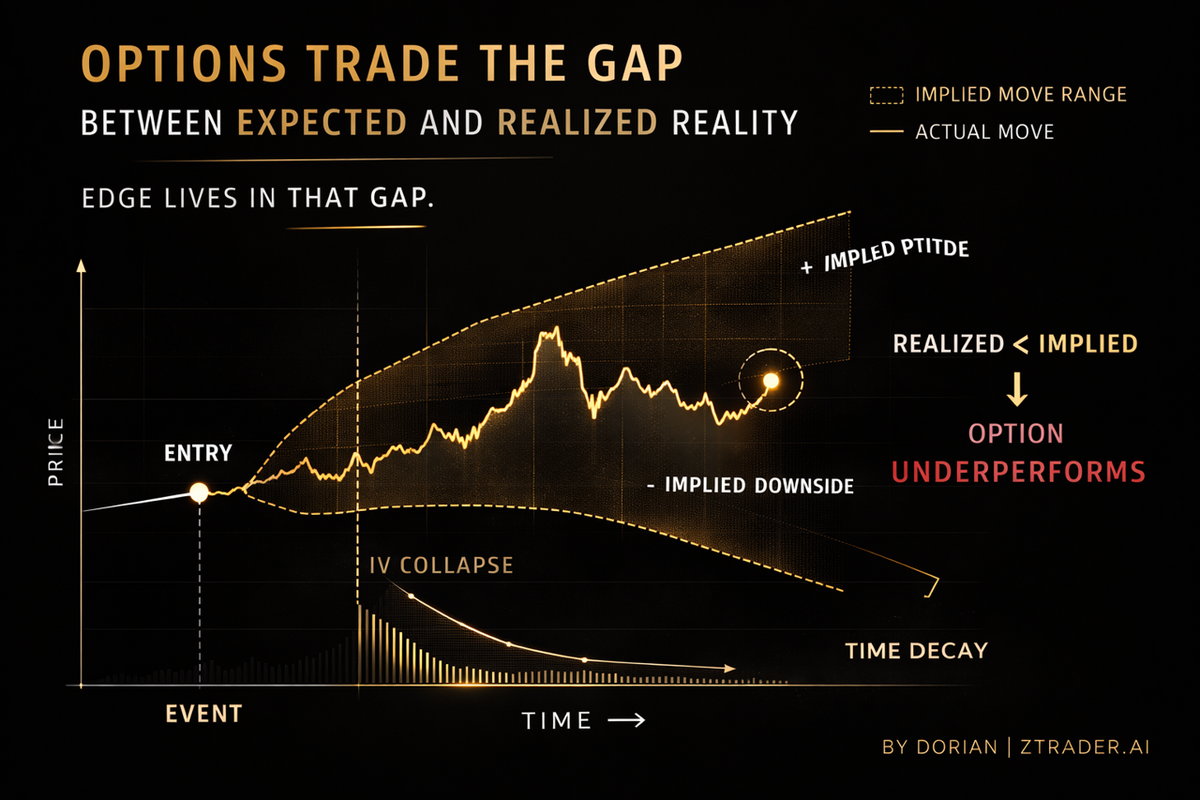

Deep Options 01 Why Being Right on Direction Is Often Not Enough Most people approach options with a stock trader’s mind. They see a market view, translate that view into a call or a put, and assume the trade will work if the underlying moves in the expected direction. If they are bullish, they buy calls. If they are bearish, they buy puts. The logic feels clean, almost obvious. A call is a levered way to express upside. A put is a levered way to express downside. In theory, it sounds efficient. In practice, this is where many options traders begin losing money. Because an option is not just a directional instrument. It is a contract whose value is jointly determined by direction, time, and implied volatility. The underlying can move in the “correct” direction and the option can still fail to produce the payoff the trader expected. Sometimes the gain is much smaller than expected. Sometimes the option barely moves. Sometimes it even loses value after the market moves in the anticipated direction. To someone who still thinks like a stock trader, this feels irrational. It is not irrational at all. It is simply the options market pricing something different from what the trader though

Premium research continues below.

Unlock to read the full report, framework, and trade path.