Deepoption02

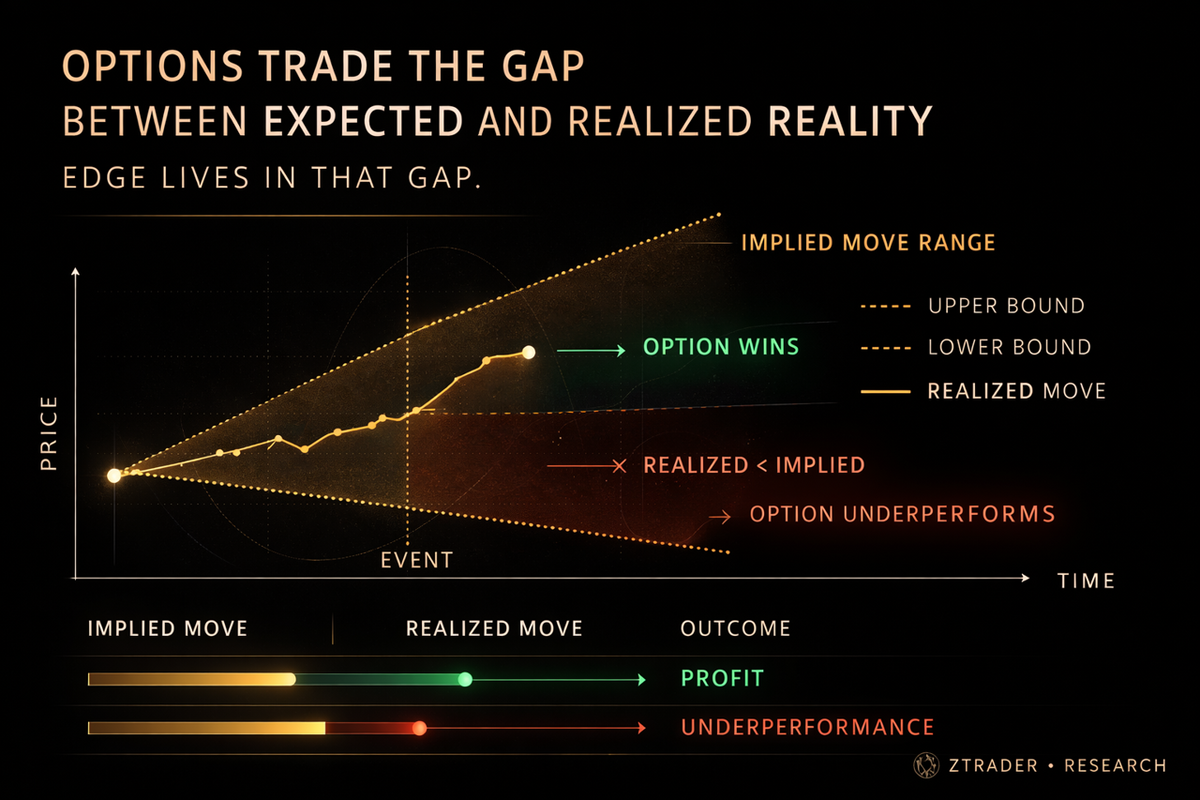

Deep Options 02 The Most Expensive Thing Retail Traders Consistently Buy There is a very specific trade that almost every developing options trader makes at some point. The setup feels logical, almost irresistible. A major event is coming. Earnings. CPI. FOMC. A product launch. A legal ruling. Something that will obviously move price. The trader thinks: volatility is coming, therefore I should buy options. What they do not realize is that this thought is already reflected in the price they are paying. The market is not surprised that an event is coming. The options market is a forward pricing machine. It does not wait for uncertainty. It prices uncertainty in advance. By the time a retail trader notices that “something big is coming,” the options market has usually been adjusting for days or weeks. Implied volatility rises not because the event happened, but because the possibility of the event exists. So what the trader thinks is anticipation is often just late participation. This is why earnings trades feel so strange the first time someone really studies them. A stock can move strongly after results and the long option buyer still feels disappointed. The move happened. The narra

Premium research continues below.

Unlock to read the full report, framework, and trade path.