This is how dollar empire is being build and designed.

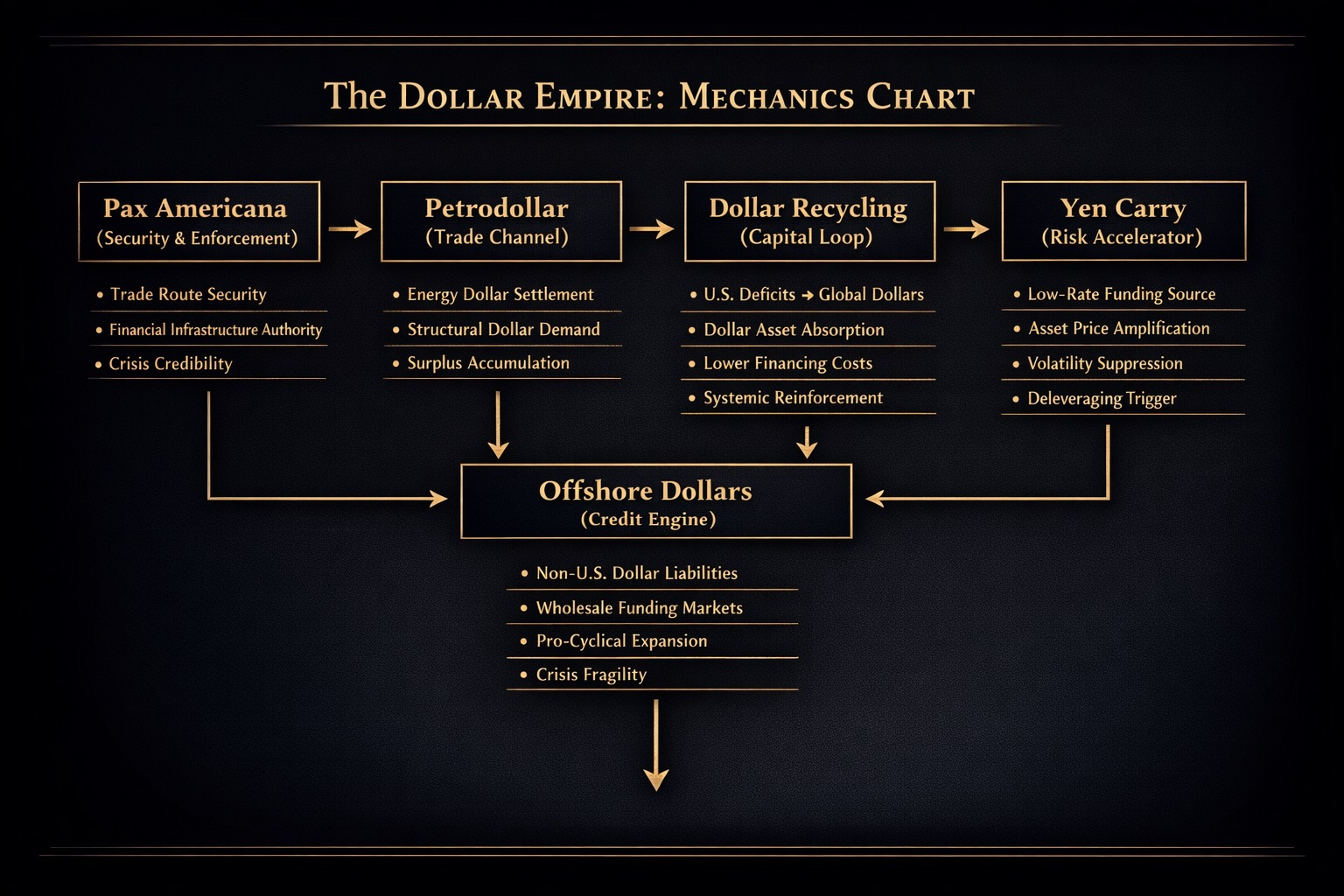

Petrodollars, Pax Americana, Offshore Dollars, Dollar Recycling, and the Yen Carry as One Integrated System Executive Premise This paper does not ask whether the US dollar is “good” or “bad,” nor does it speculate on ideological decline. It does something far more useful: It explains how the dollar system actually works as an engineered structure, why it continues to dominate global finance, and through which channels it amplifies both booms and crises. The dollar order is not sustained by belief. It is sustained by interlocking balance-sheet mechanics. Those who fail to understand this mistake symptoms for causes, and narratives for mechanisms. I. First Principles: The Dollar Order Is an Engineered System Most discussions of the dollar start from the wrong abstraction layer. They begin with: “US power” “Dollar hegemony” “Reserve currency status” These are descriptions, not mechanisms. T

Premium research continues below.

Unlock to read the full report, framework, and trade path.