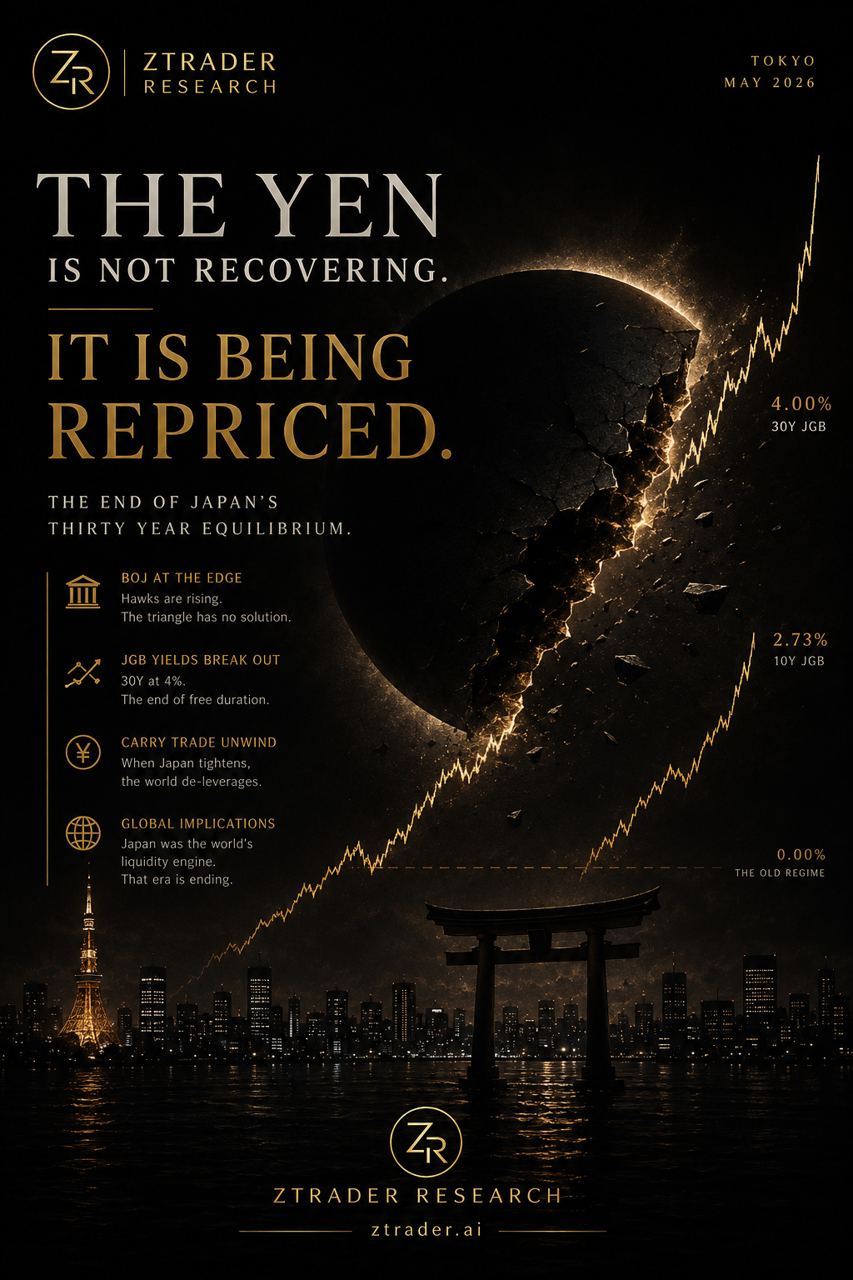

The market narrative says the yen is “stabilizing.”

Premium research continues below.

Unlock to read the full report, framework, and trade path.

ZTRADER • RESEARCH

The market narrative says the yen is “stabilizing.”

The market narrative says the yen is “stabilizing.”

Premium research continues below.

Unlock to read the full report, framework, and trade path.