Pro traders are looking at market signals/ not noises

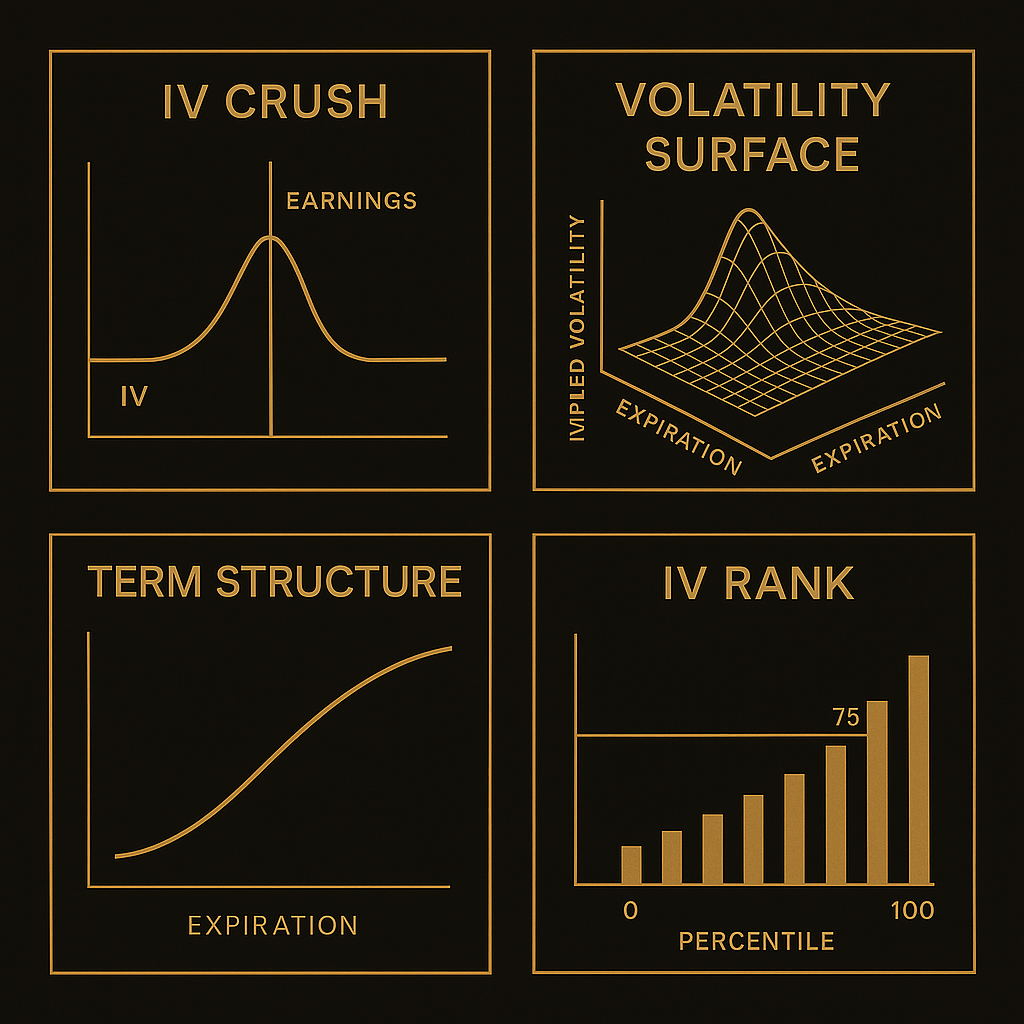

0. Prologue: Why Volatility Matters More Than Direction Most retail traders believe options are about choosing whether a stock “goes up or down.” Professionals know this is childish. Direction is only one variable. Volatility is the entire pricing engine. Time is the silent tax collector. Professionals trade distributions, not predictions. We trade variance, not vibes. We trade probability clusters, not hunches. This chapter exists to break your mind out of the directional trap and push you into the intellectual world where real PnL comes from: the world of Implied Volatility (IV). If you master IV, everything else becomes simple. If you fail to understand IV, you will always be the liquidity, never the trader. Let’s start where professionals start: with the actual drivers of option pricing. 1. What Implied Volatility Actually Represents Forget the classic textbook explanation (“IV measures expected future volatility”). That is technically correct but practically useless. Professionals view IV as: The market’s consensus on uncertainty — monetized. IV is not a forecast. IV is a price for uncertainty. When you buy an option, you’re not buying “up or down.” You’re buying the market’s

Premium research continues below.

Unlock to read the full report, framework, and trade path.